All Categories

Featured

Table of Contents

That's to protect against people from getting insurance quickly after uncovering an incurable ailment. This protection could still cover fatality from crashes and various other causes, so research the alternatives available to you.

When you aid alleviate the economic burden, household and pals can focus on looking after themselves and setting up a significant memorial rather than scrambling to discover money. With this type of insurance coverage, your recipients might not owe tax obligations on the survivor benefit, and the cash can go towards whatever they need the majority of.

Selling Final Expense Part Time

for customized entire life insurance policy Please wait while we fetch details for you. To find out concerning the items that are available please telephone call 1-800-589-0929. Change Place

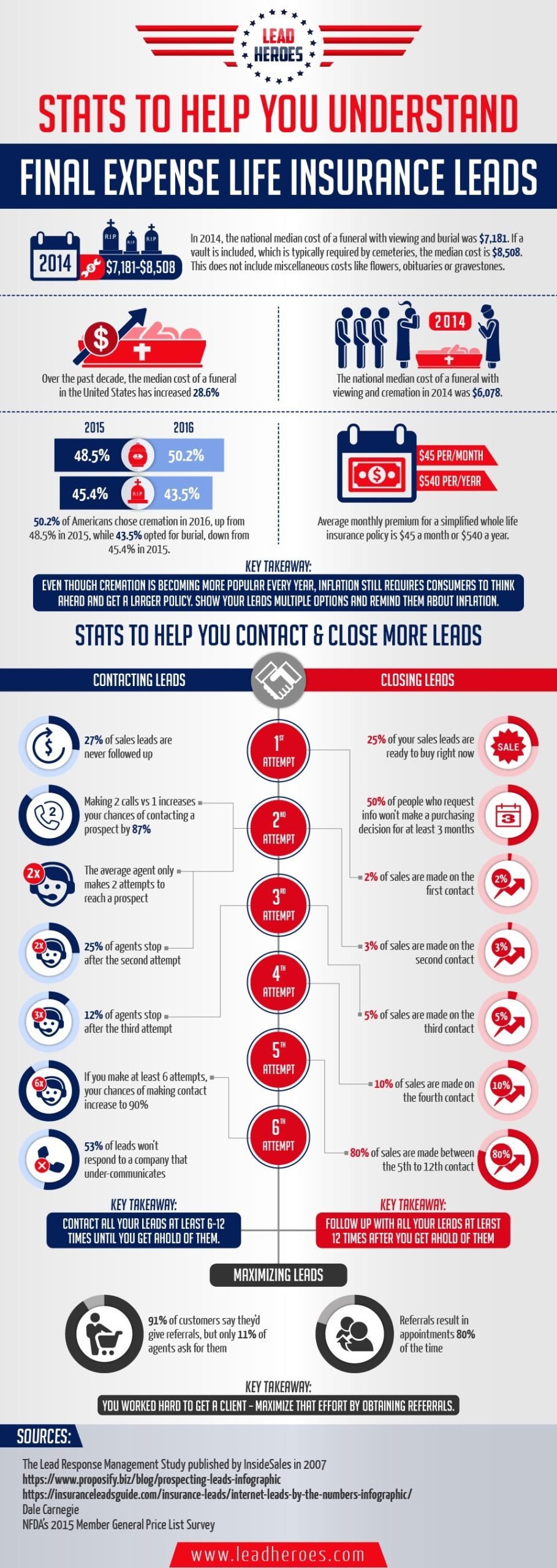

When you offer final expense insurance, you can supply your clients with the tranquility of mind that comes with knowing they and their family members are prepared for the future. Prepared to find out every little thing you need to know to start selling final expense insurance successfully?

As opposed to supplying income substitute for loved ones (like most life insurance policy policies do), final expenditure insurance is meant to cover the expenses connected with the policyholder's viewing, funeral, and cremation or burial. Lawfully, nonetheless, recipients can usually use the plan's payment to spend for anything they desire. Typically, this sort of plan is provided to people ages 50 to 85, but it can be issued to more youthful or older people also.

There are 4 primary kinds of final expenditure insurance policy: ensured issue, graded, customized, and degree (liked or common score). We'll go much more into detail concerning each of these product types, however you can gain a quick understanding of the differences in between them through the table below. Exact advantages and payment schedules may vary depending upon the provider, plan, and state.

Final Expense Insurance Training

You're assured coverage but at the highest possible rate. Generally, guaranteed problem final cost strategies are provided to customers with severe or numerous wellness concerns that would certainly stop them from securing insurance policy at a typical or graded rating. aetna burial insurance. These health and wellness problems might include (however aren't restricted to) renal condition, HIV/AIDS, organ transplant, energetic cancer cells treatments, and health problems that restrict life expectations

Furthermore, customers for this kind of strategy can have extreme lawful or criminal backgrounds. It is necessary to keep in mind that various providers provide a series of problem ages on their assured concern policies as reduced as age 40 or as high as age 80. Some will certainly additionally supply greater face worths, as much as $40,000, and others will permit much better fatality benefit conditions by improving the rate of interest with the return of premium or minimizing the number of years up until a complete fatality advantage is readily available.

If non-accidental death occurs in year 2, the service provider may only pay 70 percent of the death benefit. For a non-accidental death in year 3 or later on, the service provider would probably pay 100 percent of the fatality benefit. Modified last expense plans, comparable to graded strategies, check out wellness problems that would put your customer in a more restrictive customized strategy.

Some products have details health issues that will certainly get advantageous therapy from the carrier. For instance, there are carriers that will issue policies to younger adults in their 20s or 30s who might have persistent conditions like diabetic issues. Usually, level-benefit conventional last cost or streamlined issue whole life plans have the most affordable premiums and the largest availability of extra cyclists that clients can include to plans.

Mutual Of Omaha Burial Insurance Rates

Relying on the insurance carrier, both a favored price course and typical rate course might be provided - cheap funeral insurance. A customer in outstanding health and wellness without any present prescription medications or health conditions might get approved for a recommended price class with the most affordable costs possible. A customer healthy despite having a few upkeep medicines, yet no substantial health issues may qualify for conventional prices

Comparable to various other life insurance plans, if your clients smoke, use other types of cigarette or nicotine, have pre-existing health problems, or are male, they'll likely have to pay a higher price for a last expense plan. In addition, the older your customer is, the higher their price for a plan will be, considering that insurance companies think they're taking on more risk when they provide to insure older clients.

Family Funeral Insurance Policy

The plan will likewise continue to be in pressure as long as the policyholder pays their premium(s). While lots of other life insurance policy policies might require clinical examinations, parameds, and going to medical professional statements (APSs), last expenditure insurance plans do not.

In other words, there's little to no underwriting called for! That being stated, there are two main kinds of underwriting for final expenditure plans: streamlined problem and assured concern (final express direct). With simplified concern strategies, customers normally only have to respond to a couple of medical-related inquiries and may be refuted coverage by the provider based on those responses

Life Debit Funeral Insurance

For one, this can permit agents to find out what kind of strategy underwriting would work best for a specific customer. And two, it aids agents limit their client's choices. Some providers may invalidate customers for coverage based upon what medications they're taking and how much time or why they've been taking them (i.e., maintenance or treatment).

The brief answer is no. A final expenditure life insurance policy policy is a type of permanent life insurance policy - funeral cover with no waiting period for natural death. This implies you're covered until you pass away, as long as you have actually paid all your premiums. While this plan is designed to aid your recipient pay for end-of-life expenses, they are cost-free to use the fatality benefit for anything they need.

Similar to any kind of other long-term life plan, you'll pay a normal premium for a last expenditure policy in exchange for an agreed-upon fatality advantage at the end of your life. Each service provider has different rules and choices, yet it's relatively simple to handle as your beneficiaries will have a clear understanding of just how to invest the cash.

You may not require this type of life insurance. If you have permanent life insurance in position your final costs might currently be covered. And, if you have a term life policy, you might be able to transform it to a long-term policy without a few of the added steps of obtaining final cost coverage.

Will Life Insurance Pay For Funerals

Created to cover limited insurance policy demands, this type of insurance coverage can be a budget friendly alternative for individuals who just want to cover funeral expenses. (UL) insurance coverage continues to be in place for your entire life, so long as you pay your costs.

This option to last expenditure coverage gives options for extra family insurance coverage when you require it and a smaller sized insurance coverage quantity when you're older.

5 Important truths to remember Planning for end of life is never enjoyable (most affordable funeral plan). Neither is the thought of leaving liked ones with unexpected expenses or financial debts after you're gone. Oftentimes, these monetary responsibilities can stand up the settling of your estate. Think about these 5 realities about last expenditures and just how life insurance coverage can assist spend for them.

{kind=link}

Latest Posts

Does Health Insurance Cover Funeral Costs

Funeral Expense Insurance For Seniors

Best Funeral Plan Providers